RoC penalises Company, CS & KMPs for not maintaining serial-wise Attendance Register

- Blog|News|Company Law|

- 2 Min Read

- By Chetan Kulasri

- |

- Last Updated on 20 December, 2022

Latest from Taxmann

[2022] 145 taxmann.com 449 (Article)

1. Secretarial Standard

As per the explanation to sub-section(1) of section 205 of the Companies Act 2013, Secretarial Standards means the “Secretarial Standards” as issued by the Institute of Company Secretaries of India constituted under section 3 of the Company Secretaries Act, 1980 and approved by the Central Government. The secretarial standards provide clarity on the respective subjects and it does not mean that the secretarial standards are alternative to the original laws enacted by the Parliament. One could conclude by saying that wherever the law is not clear it requires an explicit spirit of the law, the secretarial standard provides clarity on the respective subjects to the user. As per the provisions of the Companies Act 2013, adherence by a company to the Secretarial Standard is mandatory.

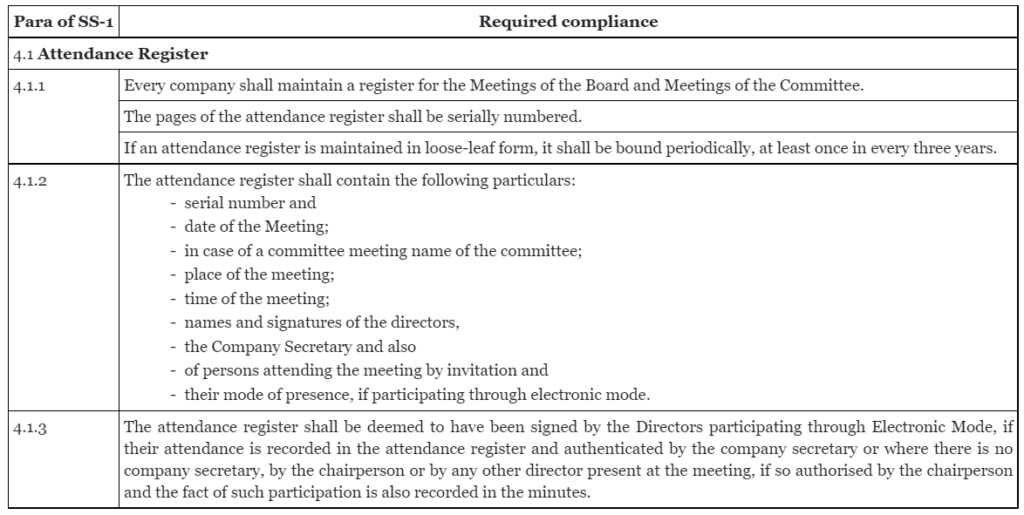

2. Attendance Registers for meetings of the board, general meetings and meetings of the committee

The Secretarial Standard-1 issued by the Institute of Company Secretaries of India, spells out in its para 4 under the heading “Attendance at Meetings” which is required to be maintained by every company. The relevant provisions relating to the maintenance of the attendance register as per the Secretarial Standard are as given below:-

3. Relevant provisions relating to Secretarial Standard under the Companies Act 2013

Sub-section (10) of section 118 of the Companies Act 2013 provides that every company shall observe Secretarial Standards with respect of general and board meetings specified by the Institute of Company Secretaries of India constituted under section 3 of the Company Secretaries Act 1980 and approved as such by the Central Government.

4. Penal provision for default/violation

Sub-section (11) section 118 of the Companies Act 2013 provides inter alia that if any default is made in complying with the provisions of section 118 in respect of any meeting, the company shall be liable to a penalty of twenty-five thousand rupees and every officer of the company who is in default shall be liable to a penalty of five thousand rupees.

5. Consequences of any default

To understand the consequences of any default while complying with the Secretarial Standards-1 and 2 relating to the meetings of the board of directors (and other meetings) mandated by the Companies Act 2013, let us go through the decided case law by the Registrar of Companies, NCT of Delhi & Haryana on this matter on 30th November 2021.

Click Here To Read The Full Article

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.