GST Registration – Suspension | Cancellation | Revocation Process Explained

- Blog|GST & Customs|

- 17 Min Read

- By Chetan Kulasri

- |

- Last Updated on 17 October, 2024

Latest from Taxmann

Table of Contents

- Overview

- Anatomy of a Notice

- Limitations of Scope

- Rejection of Application

- Repeated Applications without Reply to Notice

- Option for Composition

- Option for Provisional Assessment

- Suspension of Registration

- Suo Motu Cancellation

- Revocation of Cancellation

- Voluntary Cancellation

- Appealable Orders

- Circulars and Instructions

Check out Taxmann's How to Deal with GST Show Cause Notices with Pleadings which provides comprehensive guidance on handling GST Show Cause Notices with key features, including detailed checklists, visualisations, and over 50 real-life draft pleadings. It covers various types of notices, including system-generated and sequel notices, and provides practical tools for drafting effective responses. The book also includes strategic do's and don'ts, remediation measures under Sections 11A and 128A, and insights into the growing role of data analytics in GST assessments. Additionally, it incorporates the latest amendments from the Finance (No. 2) Act, 2024 and provides guidance on appellate proceedings and revisionary processes.

1. Overview

Registration (sections 25 and 27), suspension and cancellation (section 29), revocation (section 30) and appeal for restoration of registration (section 107) are a series of administrative actions that demand prompt response from taxpayers that involve complex ‘due process’ in Chapter VI of Central GST Act. While the rigours of notice issued in respect of any demand may not be applicable while issuing notices in relation to registration and related proceedings, but the requirement to ‘put at notice’ – the applicant or registered taxpayer – and ensure there is no miscarriage of justice is not all lost in these proceedings. Deliberation on notices in respect of registration matters is a precursor to deliberations on demand notices. And these deliberations are not an attempt at restating the statutory provisions but an invitation to consider the underlying principles and judicious analysis that notices warrant.

2. Anatomy of a Notice

Procedure for registration also affects rights of taxpayers and where there are any administrative or quasi-judicial action that can bring adverse consequences, principles of natural justice (discussed later) must be followed even if no express provision is found in the law to do so. There are significant adverse consequences of non-registration (by rejection or application or cancellation of registration) that valid registration avails.

Input tax credit is allowable to only to a ‘registered person’ but output tax may be demanded from any ‘taxable person’. Without registration, input tax credit cannot be claimed, e-waybill cannot be generated or issue tax invoice to collect GST from Customers, etc. Reference may be had to the decision of Uttarakhand High Court in Vinod Kumar v. CST (WP 1553/2021) where passionately speaking for the taxpayer, it was observed that:

“So, if the petitioner is denied a GST registration number, it affects his chances of getting employment or executing works. Such denial of registration of GST number, therefore, affects his right to livelihood. If he is denied his right to livelihood because of the fact that his GST Registration number has been cancelled, and that he has no remedy to appeal, then it shall be violative of Article 21 of the Constitution as right to livelihood springs from the right to life as enshrined in Article 21 of the Constitution of India.”

Every application is assigned to Central or State (or UT) GST department for verification and grant of registration, concerned Proper Officer must discharge duties to prevent prejudice to Revenue while acting as a ‘trade facilitator’.

Applicant is required to be ‘put at notice’ in the following situations in respect of registration:

- Deficiencies in application for registration;

- Proposal to suspend or cancel registration; and

- Justification for revocation of suspended registration.

Short point for consideration in these notices is to determine questions of fact that entail grant of registration by Proper Officer.

3. Limitations of Scope

At the time of registration, it is nearly impossible to decisively show any prejudice to Revenue (by grant of registration) as business is yet to commence. Although experience under earlier laws points to certain misadventures by registered persons, but the role of Proper Officer under section 25 is not that of an investigator and such these cannot be sufficient reasons to reject taxpayer’s application for registration:

- Applicants are benami and are acting for some other persons;

- Application is insufficient to clearly establish identity of Applicant and business premises;

- Registration threshold was already crossed earlier, and application made is to overcome investigation as ‘unregistered person’;

- Purpose of registration is to claim and transfer input tax credit;

- Incorrect category used – regular, casual, non-resident or ISD;

- Goods proposed to be dealt with are prone to evasion.

With this in mind, requirement to issue notice is to allow Applicant an opportunity to satisfy Proper Officer of correctness, completeness and reliability of documents submitted in support of the assertions made in the application. There is no investigative work involved. Applicants’ reply is to be binary, not involving complex questions of law. But it is important to recognise that notices in proceedings from section 25 are as much a ‘due process’ of law as a notice involving ‘demand’ under other provisions.

Given the limited purpose for which requirement to issue notice is mandated, it is important for Applicant to be able to understand and respond. Time limits prescribed in the ‘due process’ involved in these notices are short in view of these very limitations. Extensive investigative work is NOT involved and enquiry into pre-registration activities of Applicant is NOT permitted in law.

4. Rejection of Application

This is also a ‘decision or order’ made by the Proper Officer and for that reason, it is appealable even if it is unusual for an Applicant to pursue remedy in appeal than file a fresh application. In law, appeal against Order of Rejection is permitted under section 107(1) which demands that the grounds on which application is rejected be open for consideration by Appellate Authority. As any other proceeding involving application of mind to reach a finding on facts (or law), Order of Rejection in REG5 must be a Speaking Order (discussed later). It must state the reasons for the finding that application merits rejection, duly supported by documents or response from Applicant, which brings out the insufficiency of documentations required to establish identity or location of establishment and that of authorized persons.

Extensive enquiry into correctness of aggregate turnover, classification and forecast of turnover and nature of supplies are not germane at this stage. Rejection must be confined to the objective of application for registration. Often it is reported that applications are being rejected due to doubts about bona fides of the Applicant. It would be remarkable that financial background or level of skill to engage in business or such other criteria are given consideration to reject application. Short point for consideration in this process must not be lost sight of, and without straying from stated objective, needs to be explicit in the Order of Rejection.

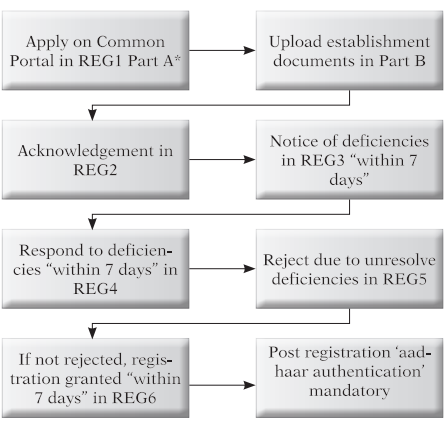

5. Repeated Applications without Reply to Notice

Application filed in REG1 Part A (within thirty (30) days on attracting liability to register or up to five (5) days in advance in case of CTP and NRTP in REG9 and separate applications in case of ISD), will be assigned on Common Portal to a Proper Officer who may be in the Central GST department or State (or UT) GST department. And where deficiencies are observed and notice issued in REG3, Applicant is obliged to respond within 7 days in REG4. Omission to respond and allowing application to lapse under rule 9(4) and filing fresh application in REG1, presents good reason to consider the ‘application history’ by the Proper Officer to whom this application is assigned.

While it may not be necessary for Proper Officer to enquire into status of any REG3 previously issued, scrutiny of current application will point to the reasons for omission to respond in REG4 in that application.

Essential information in previous application may have been misstated or incongruous with supporting documents available. But unexplained and ‘repeat applications’ involve closer verification of such applications. And when notices are issued in such cases, response may be less likely to be accepted readily. It may not be out of place to exhibit transparency in responding to notices about the reason for repeat application.

6. Option for Composition

Section 10 permits the legislative mandate to opt for composition. Rules 3 to 7 contain the ‘due process’ in this regard. Composition under section 10 is an option to be availed by a ‘registered person’. As such, there is no difference in application for registration whether taxpayer proposes to opt for composition or not. After the registration is submitted in REG1 Part B (discussed earlier), ‘intimation’ of decision to avail option to pay tax on composition basis is to be made. It is interesting that composition is an option for taxpayer which is communicated to Proper Officer by way of ‘intimation’.

Verification of application also involves limited review of ‘eligibility’ to composition and not about threshold limit of turnover, but the category of composition only, as declared by Applicant.

Example

Bakery is a manufacturer of cakes, trader in chocolates as well as service provider (eatery) in respect of items of food and soft-drinks served, which attract different rates of composition. Circular 27/1/2018-GST dated 4 Jan 2018 seems to clarify that bakery will be considered to be akin to a restaurant for purposes of composition of tax, referring to section 10(1)(b).

Notice of discrepancies in REG3 may extend to questions about Applicant’s eligibility to composition. Response to notice, even in the context of registration, entails the same level of responsibility and risk of adverse consequences as in the case of notice for demand. Clarity and transparency in response is to be maintained.

7. Option for Provisional Assessment

Section 60 permits registered persons to opt for ‘provisional assessment’ in carrying out self-assessment permitted as per section 59, soon after grant of registration or whenever the need for recourse to provisional assessment arises. Rule 98 contains the ‘due process’ in this regard. Registered Person is permitted to apply for ‘provisional assessment’ under section 60 when such person is “unable” to carry out self-assessment. Provisional assessment is not a substitute for Advance Ruling (in Chapter XVII) to redress taxpayers ‘doubts’ about interpretation of this law. Provisional assessment is a supplement to self-assessment where material information having a bearing on the self-assessment is not available, registered persons are allowed this option to seek approval in ASMT1 under rule 98 from Proper Officer to carry out assessment on provisional basis, subject of conditions.

Proper Officer’s consideration of this application has limited scope:

- maintainability of application under section 60;

- satisfaction of conditions to the grant of approval; and

- conclusion of provisional assessment.

Notice in ASMT2 is prescribed for furnishing additional information. Taxpayer’s response in ASMT3 is to firmly establish that the application is ‘maintainable’ and provisional assessment is not due to any doubts about the interpretation of this law but due to the lack of material information that has a direct bearing on the outcome in self-assessment.

Example

HSN 2306 states bran (when used as such) is animal feed, but HSN 2306 also states that bran may be put to other uses. Unless bran (residue from oil extraction) is tested in a lab, the identity of resultant product (bran) cannot be reliably known. This would be a fit case of provisional assessment, to determine if it would be exempt or taxable at 5%.

Ready-to-eat savouries sold in a sweet meat shop may be classified as supply of ‘goods’ or ‘services’. HSN code and credit restrictions are different for each. This is not a fit case for provisional assessment as the doubt is about the interpretation and not about any material fact that is not available for completing self-assessment.

While provisional assessment is not optional for Proper Officer but for taxpayer, Proper Officer is not barred from rejecting if the application is not support by good and sufficient reasons to allow the same as per law. After all, following questions involve application of mind to reach a finding on facts based on the law:

- Maintainability: whether at all, the missing information as claimed by taxpayer is mere confusion about the interpretation of law or, in fact, information that cannot be readily procured to carry out self-assessment; and

- Conditions: taxpayer is obliged to secure the interests of Revenue by executing a bond and suitable security for the differential amount of tax involved and undertake to pay such differential tax, if any, along with interest.

As approval or rejection of provisional assessment is a ‘decision or order’ it is appealable under section 107(1). Order in ASMT4 must be a Speaking Order, even if not elaborate, and must clearly state the findings and be supported by cogent reasons. Most of the information to reach this finding will flow from taxpayer’s application in ASMT1 and response in ASMT3 to notice in ASMT2.

8. Suspension of Registration

Section 29 permits suspension before cancellation of registration granted to taxpayers. Rules 21, 21A and 22 contain the due process in this regard. Cancellation of registration has some finality to it. Cancellation bars taxpayer from claiming input tax credit and issuing tax invoices. In view of the finality that cancellation involves, rule 21A permits suspension when there is delinquency by registered taxpayer in keeping all compliances current.

In view of the opportunity to reconsider and restore registration especially in an IT-based compliance environment, ‘suspension’ is now the first step in all instances whether it is due to any delinquencies or application for voluntary cancellation by taxpayer, as provided in section 29. Suspension is a pre-emptive step which DOES NOT require that a notice be issued before suspending the registration. There is no violation of principles of natural justice as there is no finality in suspension and full restitution is possible. Taxpayer will not be prejudiced either by lapse of credit or in any other manner, in case of suspension. But this exceptional and pre-emptive power cannot be exercised whimsically. It must be invoked only for good and sufficient reasons. And these reasons are expressly provided in section 29(1) and 29(2).

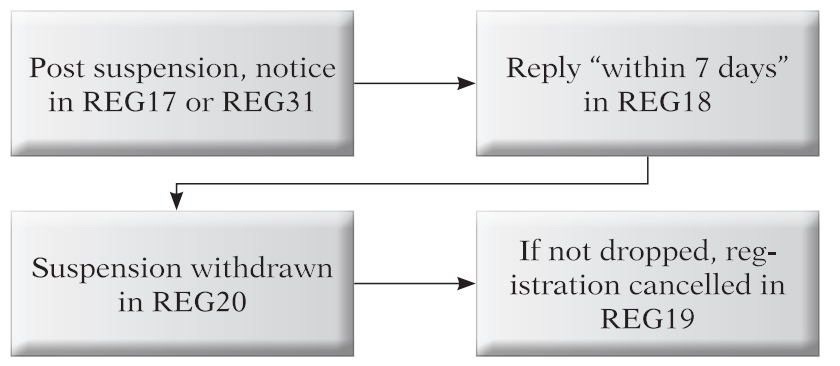

Section 29 confers jurisdiction to Proper Officer only when it can be shown that those ‘circumstances’ exist. And this is a question of fact and not one of mere guesswork. In the absence of any notice (prior to suspension of registration) it may not be possible to get full information of the reasons for suspension of registration. But the notice in REG31 will be issued ‘after’ suspension under rule 21A(2A). Such notices are ‘post decisional hearing’ notices and this is legally valid. Purpose of this notice is to put taxpayer at notice to answer the causes (for suspension and consequent cancellation) listed therein. It is important to note that the answers cannot be left without proper substantiation. And usually these answers will not entail detailed investigation and causes stated in REG31 will be self-explanatory.

Since registration is suspended and unresolved suspension can lead to cancellation, taxpayer must address causes for suspension swiftly. And this may not be the time to question jurisdiction or validity of those causes without providing material to redress delinquencies and establish need for withdrawal of suspension.

While taxpayers may have certain reasons for seeking voluntary cancellation (discussed later) or certain extenuating circumstances for allowing the registration to become delinquent (also discussed later), Proper Officer is answerable for:

- outstanding tax, interest, late fee and penalties due;

- compliance with section 29(5) in respect of credits availed.

Proper Officer is neither obliged to encourage continuation of registration nor rush to cancel registration without good reasons. Suspension may take effect from the date of application by taxpayer or as determined by Proper Officer. Suspension stops facility to issue tax invoice and collect tax, file returns, generate e-waybills, claim refund and avail other facilities on the Common Portal. Therefore, it is imperative for taxpayers to evaluate:

- need for restoration of registration;

- unsuitability of fresh registration.

In view of the relief of credit being allowed under section 18(1), there is generally no pressing need to continue the same GSTIN. There may be some ‘vendor empanelment’ changes to be made with some Customers, but the key reason for taxpayer’s strife to restore registration is to salvage unclaimed credits on ‘services’, which are not secured by section 18(1). It is well-known that response from taxpayers against suspension of registration will generally be promptly tendered, when unclaimed credit on inward supplies of services remain to be salvaged. Response from taxpayers seeking withdrawal of suspension should address all outstanding compliances of tax, interest and late fee. Where there are no further delinquencies and reason(s) for suspension properly removed, withdrawal request will not normally be denied.

Grounds such as loss of livelihood due to suspension of registration, cancellation of Contracts from Customers due to invoices not appearing in GSTR2A/2B of those Customers, etc,. are consequences that taxpayers are responsible for and not good and sufficient reasons for withdrawal of suspension. Time allowed to respond in REG18 is extended to thirty (30) in case of suspension and this time limit also indicates the time by when Proper Officer may proceed to cancel registration in REG19.

9. Suo Motu Cancellation

Section 29 permits registered taxpayers to cancel registration granted if they no longer attract the provisions of section 22 or 24, even if registration was voluntary under 25(3). Rule 21A contains the ‘due process’ in this regard. In certain specified instances, suo motu cancellation is directly permitted. Unlike suspension, cancellation is final; and for this reason, post-suspension notice in REG31 borrows from pre-cancellation notice in REG17 and response is to be furnished in REG18 within seven (7) days.

Given that Legislature has specified five (5) explicit delinquencies that taxpayers are well-informed through section 29(2) itself, there should be no violation of principles of natural justice here too by cancelling registration without serving notice. Maxim vigilantibus non dormientibus jura subveniunt states that the law assists those who are vigilant about their rights and not those who are asleep over them. And when any of these five (5) delinquencies are permitted to occur and remain unresolved, taxpayer must not express surprise or complain about ‘inadequate notice’ when Proper Officer proceeds with cancellation as authorized by Legislature.

Proper Officer is not answerable if registrations are cancelled in all cases where these specified delinquencies exist. And existence of discretion does not militate against validity of actions of Proper Officer even if adverse consequences befall taxpayers whose registrations are cancelled but no such action is taken against other taxpayers whose delinquencies are comparable. There is no right against discrimination between delinquents inter se.

Taxpayer who is issued notice in REG17 must not only reply in REG18 but more importantly redress and regularize outstanding delinquencies which formed basis for proposal to cancellation registration. And where the response and attendant redressal of all outstanding delinquencies (as mentioned in the notice) are found to be satisfactory, cancellation will be dropped by an Order in REG20. However, if the response is not satisfactory, Proper Officer is permitted to proceed with cancellation and pass a Speaking Order in REG19 and demand all dues, which extend to:

- outstanding tax, interest, late fee and penalties due;

- due under section 29(5) in respect of credits.

Very often liability under section 29(5) is lost sight of when registration is cancelled. Cancellation also entails responsibility to file final returns under section 45 within three (3) months. While these are matters to be considered by taxpayers for purposes of present deliberations, it would suffice to invite attention to these outstanding liabilities. Speaking Order in REG19 too, may omit demanding all these dues. Taxpayer’s liability on account of any of these omissions or incompleteness of demand in REG19, does not eclipse taxpayer’s liability under, say, section 29(5). The forethought in securing recovery action is evident in section 93(1) which permits recovery even from taxpayer’s estate. And even more insightful is the provision to take up determination of liability, if any, permitted long after cancellation (or even demise of taxpayer), subject only to limitation in section 74, as expressly provided in section 29(3). Cancellation does not bring down the curtains on taxpayer’s engagement with this law. Taxpayers must consider proper winding down of registration in order to be really free from liabilities coming to light later and where limitation to seek redressal by way of rectification or even appeal, may have passed.

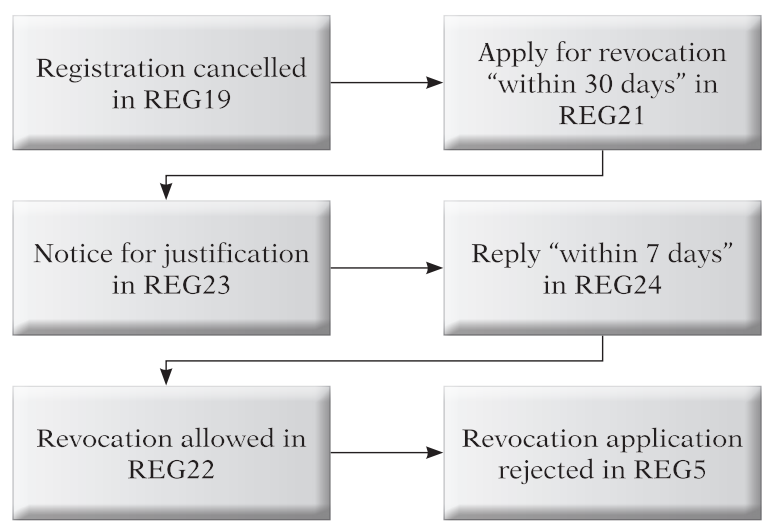

10. Revocation of Cancellation

Not even cancellation is ‘final’ because section 30 and rule 23 provide a mechanism for ‘revocation’ of cancelled registration. Real finality will come when the time limit permitted for revocation passes. However, it is noticed that taxpayer’s appeals for restoration of registration are being entertained on equitable considerations, especially citing SMWP 3/2020 of Apex Court read with notifications issued under section 168A (discussed later).

Where registration is cancelled by issuance of REG19, Proper Officer is empowered to consider application for revocation of cancellation. Although this ‘review’ appears to touch the line of violating the rule nemo judex in causa sua (discussed earlier), this power of review is express in the law (section 30) and the same is to allow relief to taxpayer, this question is unlikely to come up for consideration before Courts. Adverse outcome in violation of natural justice alone come up for consideration before Courts. Application for revocation (of cancellation) is quite straightforward and does not require elaborate pleadings as the essence of the pleading is evident in the title of the prescribed form – application for revocation of cancelled registration – to be filed. However, the justification to allow this application is important. Again here, emotional pleas for justice in view of loss of livelihood are unnecessary. Unless outstanding dues are only those that are ‘disputed and unpaid’ and outstanding compliances have been attended, a short statement would do that “said registration is still required in view of intention to continue said business”. No elaborate explanation will be required. And when it clearly shown that:

- REG21 is filed within time limit prescribed;

- all outstanding and undisputed dues have been discharged; and

- declaration that said registration is required is stated in REG24.

There would be no reason to turn down application for revocation. Proper Officer may be in a position to verify compliances online and be satisfied that application is liable to be allowed by Order in REG22. If not satisfied, Proper Officer is required to issue notice in REG23 indicating proposal to deny the request made in the application. At this time, detailed justification will become necessary, keeping in mind the possibility that any rejection of application may need to be carried in appeal and at that time the question of sufficiency of justification furnished (in adjudication proceedings) do not appear pale, deficient and impoverished. For this reason, justification in REG24 must be:

- provided within 7 days from date of service of notice in REG23;

- basis for dues left undischarged and reasons for ‘dispute’ as to the correctness of such dues; and

- declaration of the need for restoration of said registration.

Restoration of registration does not require extensive reasons to support the conclusion for application to be allowed in REG22. But to reject the application in REG5, it will require a Speaking Order. Speaking Order will furnish grounds for taxpayers to carry the matter in appeal and for Appellate Authority to see if unresolved delinquencies prevented (even a willing) Proper Officer from refusing to revoke cancellation or there were any extraneous considerations for such Order.

11. Voluntary Cancellation

Section 29 permits taxpayer to apply for cancellation of registration that is no longer required. Rule 20 contains the ‘due process’ in this regard. Care must be taken to reconfirm the basis for this determination – registration is no longer required – because output tax with interest and penalty can be demanded, limitation permitting, long after registration is cancelled but input tax credit cannot be allowed if registration stands cancelled.

Possible liabilities on cancellation of registration to consider are:

- arrears of tax, interest and penalties, if any, due;

- late fee related to monthly or annual or final returns; and

- dues under section 29(5).

Once application for cancellation in REG16 is filed, proceedings skip to the post-suspension stage along with all attendant disabilities. And where any reason to reject the application is detected, notice in REG17 and the rest of the procedure (discussed earlier) will follow until such registration is cancelled. It is often considered that registration cancelled voluntarily does not qualify for revocation (of cancellation) proceedings. But, where this is not the case, revocation is a step in the direction for redressal of grievances.

12. Appealable Orders

Revocation does not entitle reversal of all payments made under section 29(5) except to the extent credit is admissible under section 18(1). Order rejecting cancellation of registration, being an adjudication order is an appealable order and aggrieved taxpayer may prefer appeal under section 107(1). Departmental appeal is not permissible as Revenue is not aggrieved by such Order. However, when revocation is allowed in REG22, Revenue may become aggrieved due to restoration going back in time to ‘date of suspension’ and credits that had become time barred during this intervening period will become admissible with no saving provision in section 16(4). For this reason, Revenue which is aggrieved may either prefer departmental appeal under section 112(3) to Appellate Tribunal or more swiftly initiate revisionary proceedings under section 108 to set aside Appellate Authority’s Order restoring registration. Taxpayer’s rights will now be prejudiced when revisionary proceedings are initiated and effectively denying credit due to applicability of section 16(4) which was not a fact-in-issue in proceedings since suspension until revocation, before Proper Officer. Taxpayer would be able, with reasonable expectation of success, resist initiation of proceedings under section 108 due to the immediacy of prejudice to taxpayer.

13. Circulars and Instructions

Some important circulars and instructions with regard due the jurisprudence applicable to registrations are:

- Procedure for transition of registration on succession due to death of taxpayer is contained in circular 96/15/2019-GST dated 28 Mar 2019;

- Guidelines regarding revocation of cancelled registrations are contained in circular 148/4/2021-GST dated 18 May 2021; and

- Extension of time limit for revocation vide notification 34/2021-Central Tax dated 29 Aug 2021 and applicable procedures are contained in circular 158/14/2021-GST dated 6 Sept 2021.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.