Controlling – A Function of Management

- Other Laws|Blog|

- 6 Min Read

- By Chetan Kulasri

- |

- Last Updated on 27 November, 2023

Latest from Taxmann

Controlling is a primary goal-oriented function of management in an organization. It is a process of comparing the actual performance with the set standards of the company to ensure that activities are performed according to the plans and if not then taking corrective action.

Management needs to monitor and evaluate the activities at all levels. It helps in taking corrective actions by the manager, in the given timeline, in order to avoid contingencies and losses. Controlling is performed at the, upper, middle and lower levels of the management.

In this guide, you will learn the following point about controlling

- What is controlling

- Characteristics

- Objectives

- Advantages of Controlling

- Limitations

- Steps Involved in Controlling

- Types of Control

- Techniques of Controlling

1. What is Controlling

According to Brech, Controlling is a systematic exercise which is called as a process of checking actual performance against the standards or plans with a view to ensure adequate progress and also recording such experience as is gained as a contribution to possible future needs.

2. Characteristics of Controlling

- Controlling is an end function – It is a function, which comes once the performances are made in conformity with plans.

- Controlling is a pervasive function – It is a pervasive function because it is performed by managers at all levels and in all type of concerns.

- Controlling is backward as well as forward looking – Effective control is not possible without past being controlled. Controlling always look to future so that follow-up can be made, whenever required.

- Controlling is a dynamic process – Controlling requires taking revival methods, changes have to be made wherever possible. Focus has to be on controlling all the time, which makes it a dynamic function.

- Controlling is related with Planning – Planning and Controlling are two inseparable functions of management. Without planning, controlling is a meaningless exercise and without controlling, planning is useless. Planning presupposes controlling and controlling succeeds planning.

3. Objectives

- To identify the actual progress of the work in the company.

- To facilitate R&D department to improve efficiency.

- To facilitate coordination in the organization.

- To measure the actual performance with the set standard.

- To calculate the actual quantity and quality of the product.

- To eliminate wastage of resources.

- To meet the deadline of the projects.

4. Advantages of Controlling

- It helps plans to be implemented effectively.

- Controlling facilitates coordination in organizational functioning, by reducing diversity.

- It encourages high morale on the part of employees.

- It ensures order, discipline and obedience on the part of subordinates.

- Controlling helps the organization to preserve and promote its distinct identity against environmental changes.

- It makes effective use of physical and human resources, for achieving organizational goals.

- It enables organization to keep watch on external environmental for better control over it.

- Control promotes integration between Short Term Goals and Long-term Objectives Corporate Goals and Departmental Goals.

- It saves time and energy and helps in timely corrective action by the manager.

- Control allows managers to concentrate on important tasks.

- It also allows better utilization of the managerial resource.

5. Limitations

- There is difficulty in setting qualitative standards.

- There is no Control over External Factors.

- There is resistance to change from Employees.

- It is a costly affair, especially for small companies.

6. Steps in Controlling Function

Steps in Controlling Function include establishing standards, measuring performance, comparing actual performance with standard performance and finally taking remedial measures.

Figure : Steps in Controlling Function

1. Establishment of Standards – Standards are the targets required to be achieved. Controlling becomes easy through establishment of these standards because controlling is exercised on the basis of these standards. They are the criterions for judging the performance. Standards generally are classified as

-

- Measurable or Tangible Standards- Those standards which can be measured and expressed are called as measurable standards, such as cost, output, expenditure, time, profit, etc.

- Non-Measurable or Intangible Standards –These cannot be measured monetarily, such as performance of a manager, deviation of workers, their attitudes towards a concern. These are called as intangible standards.

2. Measurement of Performance – Deviations are found out by comparing standard performance with the actual performance. Performance levels are sometimes easy to measure and sometimes difficult. Measurement of tangible standards is easy as it can be expressed in units, cost, money terms, etc. Performance of a manager cannot be measured in quantities. It is also sometimes done through various reports like weekly, monthly, quarterly, yearly reports. It can be measured only by their-

| Attitude | Morale to work | Response towards physical environment |

Communication with the superiors. |

3. Comparison of Actual with Standard Performance –By comparing the actual with standard, deviations are identified. Manager has to find out whether the deviation is positive or negative or whether the actual performance is in conformity with the planned performance. The managers have to exercise control by exception.

4. Taking Remedial Actions – Once the causes and extent of deviations are known, the manager has to detect those errors and take remedial measures for it. There are two alternatives as follows:

| Taking corrective measures for deviations which have occurred | In the end, if the actual performance is not in conformity with plans, the targets are revised. |

7. Types of Control

Figure : Types of Control

1. Post-Action-Control/Feedback Control – This process involves collecting information about a finished task, assessing that information and improvising the same type of tasks in the future. The results of the completed activity are compared with pre-determined standards and if there are any deviations, corrective action can be taken for future activities. For example, a restaurant manager may ask the customer about the quality and taste of food ordered by him/her and take suggestions to improve the meals.

2. Concurrent Control – It is also called real-time control. It checks any problem and examines it to take action, before any loss is incurred.

3. Steering Control – The key feature of this control is the capability to take corrective action, when the deviation has already taken place, but the task has not been completed. The big advantage of steering control is that corrective actions can be taken early.

4. Yes/No Control – This control is designed to check at each check point, whether the allow activity to proceed further or not. These controls are necessary and useful where a product passes sequentially from one point to another, with improvements added at each step along the way. These controls stop errors from being compounded. Safety checks and legal approvals of contracts, prior to approval are examples of yes/no controls.

5. Predictive/ Feed Forward Control – This type of control helps to foresee problem ahead of occurrence. Therefore, action can be taken before such a circumstance arises.

In an ever-changing and complex environment, controlling forms an integral part of the organization.

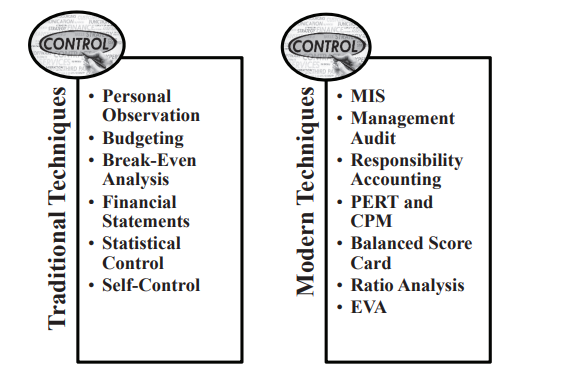

8. Techniques of Controlling

Techniques of control are being used by managers since long and there are two categories of controlling namely the traditional techniques and the modern techniques.

Figure: Techniques of Controlling

8.1 Traditional Techniques

- Personal Observation

- Budgeting

- Break-Even Analysis

- Financial Statements

- Statistical Control

- Self Control

8.2 Modern Techniques

- Management Information System (MIS)

- Management Audit

- Responsibility Accounting

- Program Evaluation and Review Technique (PERT) and Critical Path Method (CPM)

- Balanced Card

- Ratio Analysis

- Economic Value Added (EVA)

You May Also Like:

Communication- Meaning, Types and Importance in Business

Business Environment: Meaning, Characteristics and Importance

What is a Company?- Definition, Characteristics and Latest Case Laws

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.