[Analysis] Valuation and Discounted Cash Flow (DCF) Method

- Blog|Income Tax|

- 10 Min Read

- By Taxmann

- |

- Last Updated on 18 April, 2024

Latest from Taxmann

The Discounted Cash Flow (DCF) Method is a valuation technique used to estimate the value of an investment based on its expected future cash flows. This method is widely used in finance, particularly in the areas of investment analysis, financial modeling, and corporate finance. Here's a detailed breakdown of how the DCF method works: Key Components of DCF – Future Cash Flows: These are the amounts of money that an investment is expected to generate in the future. This can include earnings, free cash flow, or any other type of cash benefit expected to come from the investment. – Discount Rate: This is a rate used to convert future cash flows into present values, reflecting their worth today. The discount rate typically reflects the risk of the cash flows—the higher the risk, the higher the discount rate. Common choices for the discount rate include the weighted average cost of capital (WACC), required rates of return, or hurdle rates. – Terminal Value: At the end of the cash flow projection period, a terminal value is often calculated to account for the value of the cash flows continuing into perpetuity (or until the asset is sold). This can be done using a perpetuity growth model or an exit multiple.

By Gaurav Sukhija – National Leader (Transaction Advisory) | Kirtane & Pandit

Table of Contents

1. Valuation as a Topic

1.1 Valuation Regulatory Requirements

- Valuation for issue and transfer of shares and convertible or redeemable instruments of Indian companies under section 56 of the Income Tax Act

- Valuation for determination of capital gains tax under section 50ca of the Income Tax Act

- Valuation for indirect transfer of shares of foreign company where significant business operations lie in India under section 9 of the Income Tax Act

- Valuation for issue of shares and convertible instruments of Indian companies under Companies Act 2013

- Valuation for issue of shares and fully convertible instruments of Indian companies under RBI FDI regulations

- Valuation for acquisition/investment into shares of foreign companies under RBI ODI regulations

- Valuation M&A under section 230-232 of the Companies Act for the purposes of business combinations

- Purchase Price Allocation in case of acquisition of assets for financial reporting purposes

- Valuation for preferential allotment and takeover code as per SEBI regulations

- Valuations under SEBI alternate investment fund regulations

- Valuation of sweat equity shares

- Valuation for assets of corporate debtor (liquidation value and fair value) as per Insolvency & Bankruptcy Code

- Valuations for financial reporting purposes under IND AS (purchase price allocation, fair value under IND AS 113, impairment assessment under IND AS 36, financial instruments under IND AS 109, IND AS 32 and IND AS 107 etc.

Purpose

- Merger

- IPO

- Acquisition/Investment

- Internal Management Analsys

- Intangible Asset Valuation

Regulatory

- Income Tax Act

- SEBI

- RBI- FEMA

- Companies Act

- IBBI

Accounting

- ESOP

- Purchase Price Allocation

- Impairment Analysis

- 409(A) US ESOP Valuations

Dispute Resolution

- Company Law

- Court Order

- Mediation

- Arbitration

Fund Raise

- Issue of shares

- Transfer of shares

- Valuation for Companies Act – by Registered Valuer

- Valuation for Income tax – by Merchant Banker

- Internal Management Analysis

FEMA

- Transfer/issue of shares

- Overseas invest/divest

- Buyback/capital reduction

- Indirect transfer of shares

- Valuation by Merchant banker or Chartered Acocuntant

Income tax

- Capital gains

- Overseas transfer of/involving Indian assets

- Buyback/capital reduction

- Issuance of shares at premium

- Transfer of shares at premium or discount

- Transfer of acquisition of Intellectual property

Intangible, PPA and other accounting based valuations

- Indian GAAP/Ind AS/US/GAAP/IFRS

- Pre Deal PPA

- Post Deal PPA

- Impairment – Business/shares/intangible/goodwill

- Valuation of options/derivatives and other financial instruments including FCCBs and ESOPs

Companies Act

- Buyback/capital reduction

- Preferential allotment of shares/convertible instruments

- Issue of sweat equity/issue of shares for non cash consideration

- Mergers/Demergers/Slump sales

Portfolio Valuations

- Assessing valuation of various portfolio companies at various intervals

Model Development and Analysis

- Development of a MS-Excel Model as a deliverable

- Sensitivity analysis

- Review of a model for its logical integrity, internal consistency and arithmetical accuracy

1.2 Amendment in 11UA

For Equity shares

- NAV Book value based analysis

- DCF by Merchant banker

- PORI – Price of recent investment – VC amount < next amount

- International methods for NR

-

- Comparable Company Multiple Method;

- Probability Weighted Expected Return Method;

- Option Pricing Method;

- Milestone Analysis Method;

- Replacement Cost Methods;

For CCPS – either equity share valuation or above methods other than NAV

Special points

- Valuation is valid only for 90 days from the date of valuation report

- Consideration can be max 10% exceeding the valuation

Issues and clarifications

- NAV here can only be book value based

- Is the date of valuation report, date of signing or date of valuation?

- Funding came at 10,000 then what can be the minimum valuation?

- If funding is by both Resident and non-resident, can valuation be done by two different methods in the same report. Can there be two different valuation in same report

1.3 What is a Startup?

- Upto a period of ten years from the date of incorporation/ registration, if it is incorporated as a private limited company (as defined in the Companies Act, 2013) or registered as a partnership firm (registered under section 59 of the Partnership Act, 1932) or a limited liability partnership (under the Limited Liability Partnership Act, 2008) in India.

- Turnover of the entity for any of the financial years since incorporation/registration has not exceeded One Hundred Crore Rupees.

- Entity is working towards innovation, development or improvement of products or processes or services, or if it is a scalable business model with a high potential of employment generation or wealth creation.

1.4 Should Startup take Exemption?

It has not invested in any of the following assets,─

- building or land appurtenant thereto, being a residential house, other than that used by the Startup for the purposes of renting or held by it as stock-in-trade, in the ordinary course of business;

- land or building, or both, not being a residential house, other than that occupied by the Startup for its business or used by it for purposes of renting or held by it as stock-in-trade, in the ordinary course of business;

- Loans and advances, other than loans or advances extended in the ordinary course of business by the Startup where the lending of money is substantial part of its business;

- capital contribution made to any other entity;

- shares and securities;

- a motor vehicle, aircraft, yacht or any other mode of transport, the actual cost of which exceeds ten lakh rupees, other than that held by the Startup for the purpose of plying, hiring, leasing or as stock-in-trade, in the ordinary course of business;

- jewellery other than that held by the Startup as stock-in-trade in the ordinary course of business;

- any other asset, whether in the nature of capital asset or otherwise, of the nature specified in sub-clauses (iv) to (ix) of clause (d) of Explanation to clause (vii) of sub-section (2) of section 56 of the Act.

Provided the Startup shall not invest in any of the assets specified in sub-clauses (a) to (h) for the period of seven years from the end of the latest financial year in which shares are issued at premium

1.5 Valuation Process

- Analyse performance and historical data

- Broadly analyse the financial forecast

- Hold discussions with Management

- Conduct Industry research

- Conduct valuation using appropriate approaches

- Prepare valuation Report and discuss the results with Management

1.6 Valuation Methodologies

There are several commonly used and accepted methods for determining the value of shares/businesses, which one can apply in the present valuation exercise, to the extent relevant and applicable, such as:

Cost approach

- Net asset value (“NAV”): The asset based valuation approach is based on the underlying net assets and liabilities of the company on a book/replacement/realisable value basis.

Market approach

- Market prices method: The valuation derived from the quoted market prices of the shares of the subject company.

- Comparable companies multiples method (“CCM”): An approach that entails looking at market quoted prices of comparable companies and converting that into the relevant multiples. The relevant multiple after adjusting for factors like size, growth, profitability, etc is applied to the relevant financial parameter of the subject company.

- Comparable transactions multiples method (“CTM”): Valuation based on price paid in recent transactions which includes reviewing published data on actual transactions involving either minority or controlling interests in either publicly traded or closely held companies. Similar to comparable companies analysis, the transaction price is converted into a relevant multiple and applied, after adjustments for factors like size, growth, profitability, control etc. to the relevant financial parameter of the subject company.

Income approach

- Discounted cash flow method (“DCF”): Discounts forecasted cash flows to the present using a relevant discount rate. The discount rate, weighted average cost of capital (“WACC”) or cost of equity (“CoE”) (depending on the cash flows being used), reflect the return expectations from the asset depending on the inherent risks in the cash flows.

PWC research: The primary valuation approaches remain the income approach (discounted cash flow) and market approach (based on market multiples). The general indication from respondents is that the income approach remains the primary valuation methodology, used by 58% of respondents, while the market approach is also an important methodology, with 42% of the respondents using it as their preferred approach.

1.7 Sources of Information

The valuation analysis was undertaken on the basis of the following information relating to the Company provided to us by the Management and information available in public domain:

- Audited financial statements

- Provisional financial statements as on valuation date

- Projected profit and loss accounts of the Company for a period of five years

- Anticipated working capital requirement and the capital expenditure over the Forecast Period

- Fully dilutive Shareholding pattern as on valuation date

- Other relevant details such as history, shareholding pattern, its past and present activities, future plans and prospects and other relevant information and data

We have also received the necessary explanations, information and representations, which we believed were reasonably necessary and relevant to the present valuation exercise from the Management.

2. Discounted Cash Flow Method

The discounted free cash flow technique is one of the most detailed approaches to valuation of a business. In this technique the projected free cash flows from business operations are discounted at the weighted average cost of capital (“WACC”) and the sum of such discounted free cash flows is the value of the business.

DCF Approach

- Determine free cash flows: The future free cash flows to firm have been computed as follows:

-

- EBIT

- less: taxes

- add: depreciation and amortisation,

- add: decrease/(increase) in working capital,

- less: capital expenditure.

- Determine explicit period: Explicit Forecast Period cash flows estimated based on the business plan provided by the Management.

- Weighted Average Cost of Capital (WACC)

- Terminal value: The value during the post explicit Forecast Period, estimated using an appropriate method.

- Present value of cash flows from explicit period and terminal value discounted @ WACC

- Separate adjustments for inter alia – cash, surplus assets, etc.

- Value using DCF

3. Pillars of Discounted Cash Flow Method

3.1 Pillar 1 – Projections

- Common sizing

- Initiating coverage reports and analyst reports

- Year on year growth patterns

- Budget or target but not aspirational

- Industry trends: Specifically talking about Total addressable market, Total serviceable market, company capacity, eg. Aeroplane industry % market share, etc.

- Check whether same projections are given to investor or not

Some important terms

- TAM – Total Addressable Market

- SAM – Serviceable Addressable Market

- SOM – Serviceable Obtainable Market

- CAC – Customer acquisition cost

- RoAS – Return on ad spend

Pillar 1 – FCFF (Free Cash Flow to Firm ) or FCFE (Free Cash flow to Equity)

The key difference between Unlevered Free Cash Flow and Levered Free Cash Flow is that Unlevered Free Cash Flow excludes the impact of interest expense and net debt issuance (repayments), whereas Levered Free Cash Flow includes the impact of interest expense and net debt issuance (repayments).

Discounting Method

- FCFF- WACC

- FCFE – Cost of equity (Ke)

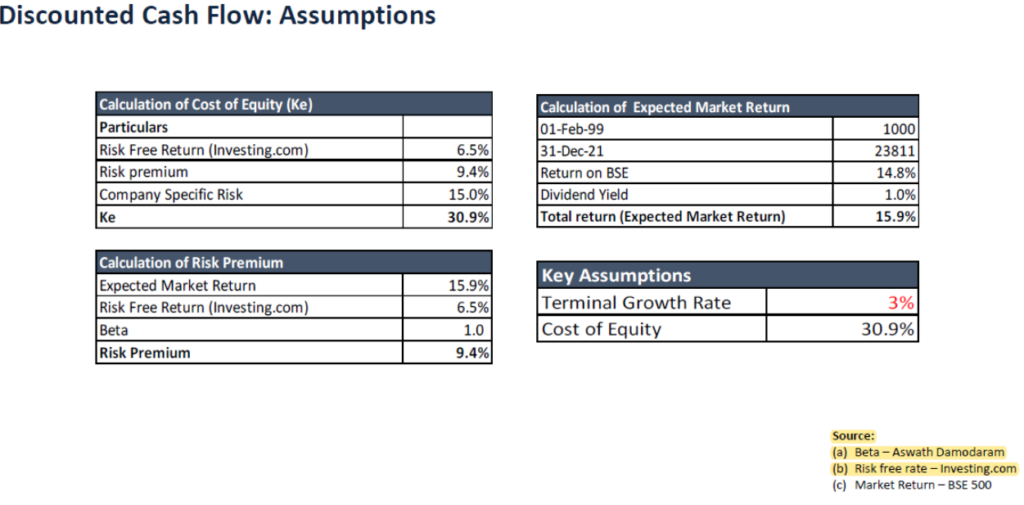

3.2 Pillar 2 – Discount Rate

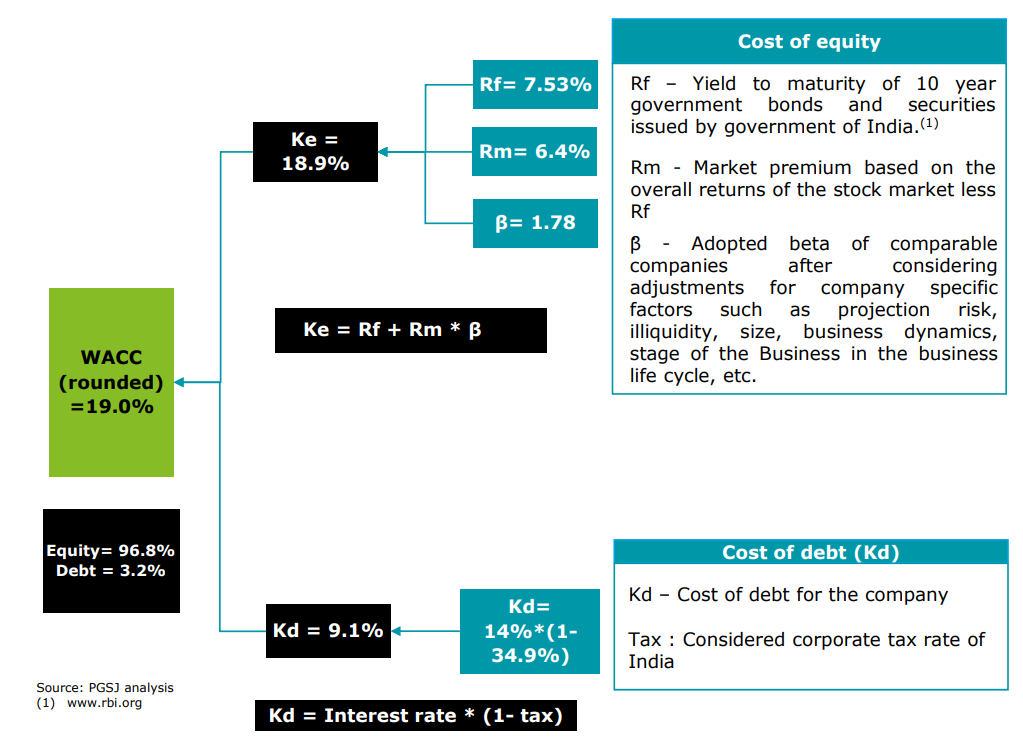

- WACC is a rate of return that an investor would expect to receive if capital were invested in a similar venture.

- The WACC, which is the weighted average of the costs of equity and debt of the business, has been worked out as follows:

WACC = Ke (e/(d+e)) + Kd(d/(d+e)), where:

- Ke represents the cost of equity, i.e. the return required by equity shareholders;

- Kd represents the after-tax cost of debt, i.e. the return required by debt holders;

- e represents the value of equity; and

- d represents the value of debt.

Minority Discounts

- The minority discount relates to the lack of control that minority shareholders have over the operation and corporate policy of a given investment.

- Ranges between 10% to 25%

Control Premium

- Control premium relates to the additional value associated with the ability to control the distribution of cash generated by a company, which includes the ability to influence the timing and size of its dividend distribution.

- Ranges between 10% to 33%

Discount for size margin and business dynamics

- It is comparing our subject company to comparable companies

- Ranges between 25% to 50%

Discount for lack of Marketability

- Marketability can be defined as ‘the ability to convert the business ownership interest (at whatever ownership level) to cash quickly, with minimum transaction and administrative costs in so doing and with a high degree of certainty of realising the expected amount of net proceeds

- Ranges between 20% to 60%

3.3 Pillar 3 – Terminal Value

- Gordon Growth Method: The Gordon growth model (GGM) is a formula used to determine the intrinsic value of a stock based on a future series of dividends that grow at a constant rate.

- H model: The H-model is a quantitative method of valuing a company’s stock price. The model is very similar to the two-stage dividend discount model. However, it differs in that it attempts to smooth out the growth rate over time, rather than abruptly changing from the high growth period to the stable growth period. The H-model assumes that the growth rate will fall linearly towards the terminal growth rate.

- Exit Multiple Method: The method assumes that the value of a business can be determined at the end of a projected period, based on the existing public market valuations of comparable companies.

3.4 Pillar 4 – After Adjustments

- Fully diluted shareholding pattern

- Cash

- Investments

- Debt

- Debt like items

- Land – surplus assets

Valuation Methodologies

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.

Taxmann Publications has a dedicated in-house Research & Editorial Team. This team consists of a team of Chartered Accountants, Company Secretaries, and Lawyers. This team works under the guidance and supervision of editor-in-chief Mr Rakesh Bhargava.

The Research and Editorial Team is responsible for developing reliable and accurate content for the readers. The team follows the six-sigma approach to achieve the benchmark of zero error in its publications and research platforms. The team ensures that the following publication guidelines are thoroughly followed while developing the content:

- The statutory material is obtained only from the authorized and reliable sources

- All the latest developments in the judicial and legislative fields are covered

- Prepare the analytical write-ups on current, controversial, and important issues to help the readers to understand the concept and its implications

- Every content published by Taxmann is complete, accurate and lucid

- All evidence-based statements are supported with proper reference to Section, Circular No., Notification No. or citations

- The golden rules of grammar, style and consistency are thoroughly followed

- Font and size that’s easy to read and remain consistent across all imprint and digital publications are applied