All-About Maharashtra Stamp Duty Amnesty Scheme – Benefits | Processes | Practical Insights

- Other Laws|Blog|

- 6 Min Read

- By Chetan Kulasri

- |

- Last Updated on 7 March, 2024

Latest from Taxmann

By Adv. Shyamsundar Patil, IAS (Rtd) – Former MD | Mahananda, CA. Ramesh Prabhu – Chairman and CA. Shreyash Prabhu – Chairman | Maharashtra Societies Welfare Association (MahaSewa)

Table of Contents

- What is Stamp Duty?

- Why to pay Stamp Duty?

- When to pay Stamp Duty?

- Instruments on which stamp duty applicable

- Significance of year: 1958 – 1980 – 1985

- Stamp Duty on Gift deed

- Stamp Duty Amnesty Scheme 2023 – 2024

1. What is Stamp Duty?

- It is a tax payable to the STATE GOVERNMENT

- Payable under Section 3 of The Maharashtra Stamp Act, 1958

- Payable on Instruments given under Schedule-I of the Act

- Only on proper payment of stamp duty is an instrument admissible as evidence in Court

- Stamp duty to be paid in Full and On Time

- Delay of payment of stamp duty attracts Penalty

2. Why to pay Stamp Duty?

- It is to be paid as LAW exists

- To ensure Legal Validity of Document

- As per Sec 34, Instrument not duly stamped is inadmissible as evidence

- If not paid, under sec 34 Penalty of 2% per month from date of signing till deficient stamp duty is paid

- Penalty up to 400% i.e. 4 times

If penalty is not paid, then?

- Confiscation

- Land Seizure

- Under Sec 59(1) of Maharashtra Stamp Act, 1958 Imprisonment for a term NOT LESS THAN 1 month which may extend to 6 months

3. When to pay Stamp Duty?

Stamp duty payable:

- Before execution of document

- On day of execution of document

- On next working day of execution of document

4. Instruments on which stamp duty is applicable

All Instruments provided in Schedule I of Maharashtra Stamp Act, 1958.

| Article | Name of Instrument |

| Art 5 | Agreement |

| Art 10 | Articles of Association of companies |

| Art 25 | Conveyance |

| Art 34 | Gift |

| Art 52 | Release Deed |

Total 63 different types of instruments are covered in the schedule

5. Significance of year: 1958 – 1980 – 1985

11th June, 1958:

- Bombay Stamp Act, 1958 came into effect which was later changed to Maharashtra Stamp Act, 1958 in the year 2015.

4th July, 1980:

- Market value concept was introduced.

- Stamp duty payable on market value or agreement value whichever is higher.

- Earlier stamp duty payable on agreement value only.

10th December, 1985:

- Stamp duty payable compulsory on Agreement for sale

- Before that only Rs. 5 required and stamp duty payment required during agreement for sale

| Stages | Period | Article – Schedule I | Stamp duty Rate/Amount (Rs.) |

| A. | From beginning of Maharashtra Stamp Act, 1958 till 9.12.1985 | ||

| 1st Stage | At the time of execution of Agreement for sale

Important Note: There was no provision to collect stamp duty leviable on conveyance at the time of agreement for sale. |

5(h) | Rs. 5 |

| 2nd Stage | At the time of Execution and registration of the conveyance deed or sale deed in the name of the society or the purchaser.

Important Note: Thus full stamp was required to be paid at the time of conveyance and not at the time of agreement. Thus, there was a provision to postpone the liability of payment of stamp duty till the conveyance deed is executed. |

25 | i) Upto market value of Rs. 50,000/- at 10%

ii) Between Market value of Rs. 50,010 to Rs.1,00,000/- at 12% of the value. iii) Above Rs,1,00,000/- at 15% of the value. |

| B. | After 10.12.1985 | ||

| 1st Stage | At the time of execution of Agreement for sale

Important Note: The provision was made to collect the stamp duty applicable on conveyance at the time of agreement for sale only by inserting the explanation 1 to the Article 25. Each agreement for sale was considered as part Conveyance. |

Explanation 1 to Article 25 | Stamp duty is payable as part of deemed conveyance |

| 2nd Stage | At the time of Execution and registration of the conveyance deed or sale deed in the name of the society or the purchaser.

Important Note: Since applicable stamp duty on conveyance was paid at the time of agreement for sale itself, at the time of conveyance nominal stamp duty of Rs.100- per flat is payable at the time of execution and registration conveyance deed |

Proviso to Explanation 1 to Article 25 | Nominal stamp duty of Rs.100/- per flat only. |

10th December, 1985:

Eg: Building constructed in 1983 having 100 members and conveyance of building to society done in 2023

80 members bought flat in 1983:

In 1983 – Had to pay Rs.5 as stamp duty applicable.

In 2023 – Have to pay stamp duty as applicable

20 members bought flat in 1987:

In 1987 – Had to pay stamp duty rate applicable.

In 2023 – Have to pay Rs.100 only for deemed conveyance.

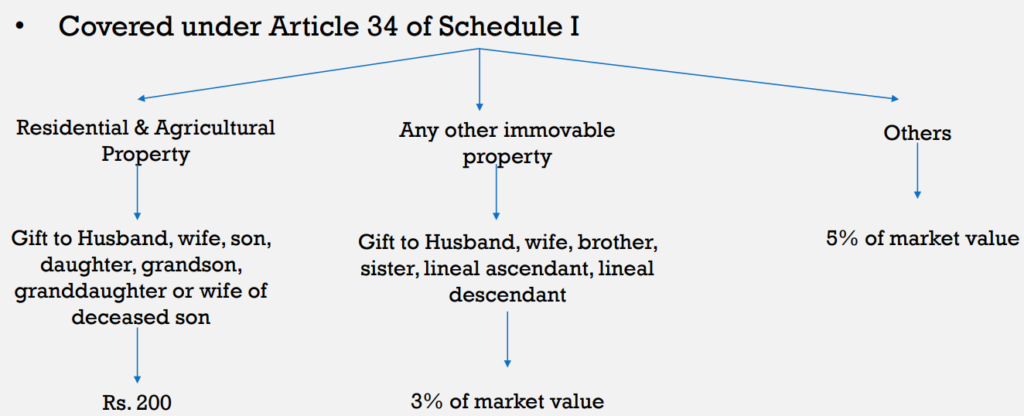

6. Stamp Duty on Gift deed

NOTE: 1% metro cess charged additional applicable since 8-2-2019

7. Stamp Duty Amnesty Scheme 2023 – 2024

7.1 What is the meaning of Amnesty?

- Forgiveness

- Pardon

- Relief

- Waiver

Revenue and Forest department of Maharashtra has introduced Amnesty scheme to reduce stamp duty and penalties on specified instruments Previous scheme was launched in 2019

7.2 When was the scheme launched?

Stamp Duty Amnesty Scheme 2023 was introduced and declared by the Govt. of Maharashtra on 7th December, 2023 via Govt order:

Mudrank-2023/C.R.No.342/M-1(Policy)

7.3 Time period for availing benefits

Scheme was launched in Two Phases for agreements between 1st January 1980 – 31st December 2020

- PHASE 1: From 1st December 2023 to 31st January 2024 – 29th February, 2024

- PHASE 2: From 1st February 2024 to 31st March 2024 – 1st March, 2024

Extended on 31st Jan, 2024 by Deputy Secretary – Shri Satyanarayan Bajaj

7.4 Instruments covered under this scheme

- Instrument related to Conveyance

- Agreement to sale

- Lease

- Sale Certificate

- Gift

- Agreement related to deposit of:

-

- Title deeds

- Pawn

- Pledge

- Hypothecation

For Residential/Non–Residential/Industrial use

- Agreement or Memorandum of agreement relating to transfer of immovable property for purpose of residential use

- Conveyance of allotment of residential/non-residential units from MHADA, CIDCO and SRA to slum dweller for purpose of rehabilitation under scheme

- Conveyance of allotment of residential/non-residential units or houses in registered Co-op Housing Societies or any apartment whose Deemed Conveyance is pending

- Any type of Development Agreement

- Conveyance

- Agreement to sell

- Instrument of transaction of Assignment of developer rights

Related to redevelopment of any dilapidated old buildings or immovable property whose redevelopment is necessary

Any type of document related to:

- Amalgamation

- Merger

- Demerger

- Arrangement

- Reconstruction of companies

Any type of instrument executed by:

- MHADA and its divisional board

- CIDCO

- Municipal Corporation

- Municipal Council

- Nagar Panchayat

- Planning authorities like MIDC, SRA, etc.

First Allotment Letter or Share Certificate issued related to residential/non-residential units by Regd. Coop. Society on Government Land or by:

- MHADA

- CIDCO

- Municipal Corporation, Council or Nagar Panchayat

- Approved planning authorities like MIDC, SRA, etc.

7.5 Benefits of the Scheme

If Instrument between

1st Jan 1980 – 31st Dec 2000 (Schedule – I)

Phase I: From 1st December, 2023 to 29th February, 2024

|

Sr. No. |

Stamp duty paid/payable | Reduction in stamp duty to be paid/payable |

Reduction in penalty to be paid/payable |

|

1 |

Rs. 1 – Rs. 1,00,000 | 100% (0% to be paid) |

100% (0% to be paid) |

| 2 | More than Rs. 1,00,000 | 50% (50% to be paid) |

100% |

If Instrument between

1st Jan 1980 – 31st Dec 2000 (Schedule – I)

Phase II: From 1st March, 2024 to 31st March, 2024

| Sr. No. | Stamp duty paid/payable | Reduction in stamp duty to be paid/payable | Reduction in penalty to be paid/payable |

|

1 |

Rs. 1 – Rs. 1,00,000 | 80% (20% to be paid) |

80% (20% to be paid) |

|

2 |

More than Rs. 1,00,000 | 40% (60% to be paid) |

70% |

If Instrument between

1st Jan 2001 – 31st Dec 2020 (Schedule – II)

Phase I: From 1st December, 2023 to 29th February, 2024

|

Sr. No. |

Stamp duty paid/payable | Reduction in stamp duty to be paid/payable |

Reduction in penalty to be paid/payable |

|

1 |

Rs. 1 – Rs. 25,00,00,000 (25 Crores) | 25% (75% to be paid) |

Penalty < Rs.25,00,000 (25 Lacs) 90% waived off Penalty >= Rs. 25,00,000 (25 Lacs) Rs. 25 Lacs to be paid, rest waived off |

|

2 |

More than Rs. 25,00,00,000 (25 Crores) | 20% (80% to be paid) |

Rs. 1,00,00,000 (1 Crore) to be paid, rest waived off |

If Instrument between

1st Jan 2001 – 31st Dec 2020 (Schedule – II)

Phase II: From 1st March, 2024 to 31st March, 2024

|

Sr. No. |

Stamp duty paid/payable | Reduction in stamp duty to be paid/payable |

Reduction in penalty to be paid/payable |

|

1 |

Rs. 1 – Rs. 25,00,00,000 (25 Crores) | 20% (80% to be paid) |

Penalty < Rs.50,00,000 (50 Lacs) 80% waived off Penalty >= Rs. 50,00,000 (50 Lacs) Rs. 50 Lacs to be paid, rest waived off |

|

2 |

More than Rs. 25,00,00,000 (25 Crores) | 10% (90% to be paid) |

Rs. 2,00,00,000 (2 Crores) to be paid, rest waived off |

7.6 General FAQs

FAQ 1. What documents need to be submitted along with application for availing amnesty scheme?

- Original Instrument on which some amount of stamp duty paid or specified allotment letter issued by authorities or CHS on Government land

- Copy of Society Registration Certificate

- Copy of BMC Assessment bill

- Copy of IOD/CC/OC of building

- Copy of Property Card

- Copy of Share Certificate (front & back)

- Copy of Aadhar Card & Pan Card along with 2 recent passport size photographs

- Letter from society about details of flat/apartment

- Authority Letter

- Proof of having possession, like:

-

- Electricity bill

- Entry in Form A during society formation

- Telephone bill

- Passport

- Election Card

- Bank Passbook

FAQ 2. My agreement is on a piece of paper (without stamp paper), can I avail the benefit?

- NOT ELIGIBLE for Amnesty Scheme

- Any amount of stamp paper should be present

FAQ 3. If stamp duty and penalty paid before the Scheme was announced, can I claim refund?

NO REFUND shall be granted

FAQ 4. How to apply for Scheme and within how many days to do the payment?

- Application to be made through Online mode through https://igrmaharashtra.gov.in website

- Within 7 days of receipt of demand notice from Registrar, payment has to be made

FAQ 5. How to tell if stamp paper is real or fake?

We have to submit application to proper authority to verify the stamp paper along with the Original Copy of the instrument requesting to verify the stamp. The appropriate authority issues a certificate as the case may be.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.