Section 194R TDS – TDS on Benefits and Perquisites

- Blog|Income Tax|

- 12 Min Read

- By Chetan Kulasri

- |

- Last Updated on 12 May, 2025

Latest from Taxmann

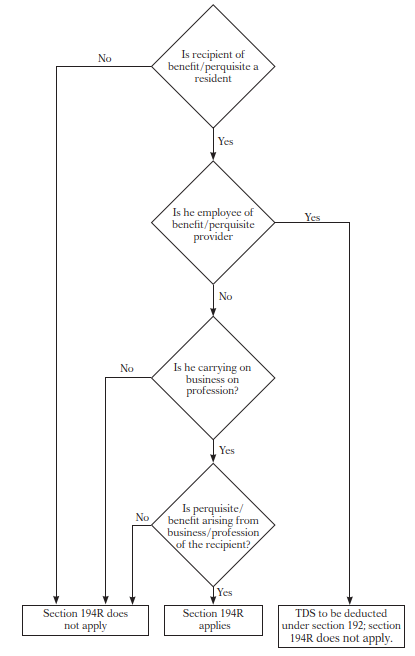

Section 194R of the Income-tax Act, 1961 mandates that any person providing a benefit or perquisite (whether in cash or in kind, or partly in both) arising from business or the exercise of a profession to a resident recipient, must deduct tax at source (TDS) at the rate of 10% before providing such benefit or perquisite.

Table of Contents

- Who Should Be the Recipient of the Benefit/Perquisite to Trigger Obligation Under Section 194R(1)?

- Recipient Should Not Be an Employee of Provider of Benefit/Perquisite

- Recipient Must Be Carrying on Business/Profession

Check out Taxmann's TDS on Benefits or Perquisites under Section 194R which is updated by the Finance Act 2025—provides an in-depth guide on TDS obligations for benefits or perquisites under Section 194R, in tandem with Section 28(iv). It clarifies valuation norms, thresholds, and exemptions supported by CBDT guidelines, illustrative case studies, and FAQs. Readers gain step-by-step insights on handling a range of scenarios—from free samples and loan waivers to brand ambassador gifts—while ensuring full compliance. Structured into foundational, advanced, and practical guidance chapters, plus an alphabetical reckoner, it is an indispensable reference for tax professionals, CFOs, and businesses.

1. Who Should Be the Recipient of the Benefit/Perquisite to Trigger Obligation Under Section 194R(1)?

From a perusal of section 194R, and the opening para of CBDT’s Circular No. 12/2022 and CBDT’s reply to Question No. 4 in the said Circular, it is clear that obligation under section 194R is triggered if the benefit or perquisite is provided to a resident person(recipient/payee) who satisfies the following conditions –

(i) Recipient is not employee of the provider of benefit or perquisite

(ii) Recipient must be carrying on business or exercising a profession or at least engaged in adventure in the nature of trade. Additionally, in view of the ratio of various judicial decisions, the following requirement should also be satisfied –

(iii) Recipient must have a business/professional relationship with provider of benefit/perquisite

If conditions in (i) to (iii) are satisfied by the resident recipient of perquisite or benefit, the “deductor” (provider of benefit/perquisite) is required to fulfil the obligation cast upon him by section 194R. So long as conditions (i) to (iii) are satisfied, liability of deductor under section 194R is triggered irrespective of who actually avails the benefit/perquisite or uses it by virtue of any connection/relationship with recipient.

2. Recipient Should Not Be an Employee of Provider of Benefit/Perquisite

Resident recipient should not be employee of provider of benefit/perquisite. If an employer-employee relationship exists between the provider and the recipient, the tax is deductible under section 192 and not under section 194R. If hospital provides any benefit/perquisite to doctor who is employee, then TDS is deductible under section 192. If hospital provides benefit or perquisite to a consultant doctor (with whom there is ‘contract for services’ and not “contract of services”), TDS is deductible under section 194R.

Now question arises what is the legal position where a free medical sample is provided by a pharma company to a doctor who is an employee of the hospital? Will the position be different if free medical sample is provided to consultant doctor of a hospital?

Question No. 4 of CBDT’s Circular 12/2022, dated 16.06.2022 clarifies under –

“.….It is further clarified that these TDS on benefits or perquisites may be used by owner/director/employee of the recipient entity or their relatives who in their individual capacity may not be carrying on business or exercising a profession. However, the tax is required to be deducted by the person in the name of recipient entity since the usage by owner/Director/Employee/relative is by virtue of their relation with the recipient entity and in substance the benefit/perquisite has been provided by the person to the recipient entity. To illustrate, the free medicine sample may be provided by a company to a doctor who is an employee of a hospital. The TDS under section 194R of the Act is required to be deducted by the company in the hands of hospital as the benefit/perquisite is provided to the doctor on account of him being the employee of the hospital. Thus, in substance, the benefit/perquisite is provided to the hospital. The hospital may subsequently treat this benefit/perquisite as the perquisite given to its employees (if the person who used it is his employee) under section 17 of the Act and deduct tax under section 192 of the Act. In such a case it would be first taxable in the hands of the hospital and then allowed as deduction as salary expenditure. Thus, ultimately the amount would get taxed in the hands of the employee and not in the hands of the hospital. Hospital can get credit of tax deducted under section 194R of the Act by furnishing its tax return. It is further clarified that the threshold of twenty thousand rupees in the second proviso to sub-section (1) of section 194R of the Act is also required to be seen with respect to the recipient entity. Similarly, the tax is required to be deducted under section 194R of the Act if the benefit or perquisite is provided to a doctor who is working as a consultant in the hospital. In this case the benefit or perquisite provider may deduct tax under section 194R of the Act with hospital as recipient and then hospital may again deduct tax under section 194R of the Act for providing the same benefit or perquisite to the consultant. To remove difficulty, as an alternative, the original benefit or perquisite provider may directly deduct tax under section 194R of the Act in the case of the consultant as a recipient.”

2.1 Test of Existence/Non-Existence of Employer-Employee Relationship Between Deductor (Provider) of Benefit/Perquisite and Recipient

TDS is deductible in respect of perquisite/benefit under section 192, and not under section 194R, when relationship of employer-employee exists between the provider of perquisite/benefit and the recipient.

The following points are noteworthy –

- In order to attract TDS u/s 192, payee (recipient) should be an individual who is an ex-employee or present employee or prospective employee.

- If the payee is a person other than individual (e.g. firm/LLP/HUF/company), then the payment can attract TDS under section 194C or section 194D or section 194G or section 194H or section 194J or section 194M or section 194R but not under section 192.

- If payee is an individual and the relationship between payer and payee is not employer-employee but client-independent contractor/service provider, then payment would not attract TDS under section 192 but may be liable for TDS under section 194C or section 194D or section 194G or section 194H or section 194J or section 194M or section 194R.

Halsbury’s Laws of England (4th edition, Vol. 16, Para 501) specifies four indicia of a contract of services –

(1) the employer’s power of selection of his employee,

(2) the payment of wages or other remuneration,

(3) the employer’s right to control the method of doing work; and

(4) the employer’s right of suspension and dismissal. However, Halsbury’s Laws also notes that none of the above tests are of universal application.

Where superior staff with professional qualifications are employed, such as senior hospital staff, eminent journalists, the employer can have little control on what work the employee is to do and no control at all in the manner in which it is to be done. In other cases, the employer may have complete control over the manner in which a worker is to work for him and the work may be of a kind usually done by employees, but the worker may nevertheless be an independent contractor and in such cases may be known as a ‘labour only sub-contractor’.

In Ram Parshad v. CIT [1972] 86 ITR 122, the Supreme Court held that for ascertaining whether a person is a servant or an agent, a rough and ready test is whether under the terms of his employment the employer exercises a supervisory control in respect of the work entrusted to that person. A servant acts under the direct control and supervision of his master. An agent on the other hand, in the exercise of his work, is not subject to the direct control or supervision of the principal, though he is bound to exercise his authority in accordance with all lawful orders and instructions which may be given to him from time to time by his principal. However, the above test is not universal in its application. A person who is engaged to manage a business may be a servant or an agent according to the nature of his service and the authority of his employment. Generally it may be possible to say that the greater the amount of direct control over the person employed, the stronger is the conclusion in favour of his being a servant. Similarly, the greater the degree of independence the greater the possibility of the services rendered being in the nature of principal and agent. It is not possible to lay down any precise rule of law to distinguish one kind of employment from the other. The nature of the particular business and the nature of the duties of the employee will require to be considered in each case in order to arrive at a conclusion as to whether the person employed is a servant or an agent. In each case the principle for ascertaining remains the same.

In Lakshminarayan Ram Gopal & Son Ltd. v. Govt. of Hyderabad [1954] 25 ITR 449 (SC), it was held that the distinction between a servant or an agent can be summarised as follows –

(i) generally a master can tell his servant what to do and how to do it;

(ii) generally a principal cannot tell his agent how to carry out his instructions;

(iii) a servant is under more complete control than an agent;

(iv) generally, a servant is a person who not only receives instructions from his master but is subject to his master’s right to control the manner in which he carried out those instructions; an agent receives his principal’s instructions but is generally free to carry out those instructions according to his own discretion;

(v) generally a servant qua servant has no authority to make contracts on behalf of his master; generally, the purpose of employing an agent is to authorise him to make contracts on behalf of his principal;

(vi) generally an agent is paid commission upon effecting the result which he has been instructed by his principal to achieve;

(vii) generally a servant is paid wages or salary.

As noted in Halsbury’s Laws of England and by the Supreme Court in Ram Parshad v. CIT [1972] 86 ITR 122, the test of whether employer’s complete control over work be done and the manner of its execution cannot decide in all cases whether the person hired is his employee/servant or an independent contractor/professional. This problem especially arises in the matter of doctors appointed as consultant doctors by hospitals. Often, disputes arise between the assessee-hospitals and income-tax department as to whether the payments by hospitals/polyclinics to doctors are ‘salaries’ liable to TDS under section 192 or ‘payments for professional services’ liable to TDS under section 194J. Now, such dispute will arise in the context of deduction of TDS on benefits or perquisites provided by hospital to its doctors. These consultant doctors are eminent professionals in their fields of specialisation and the “control and supervision by employer” test fails.

It must be noted that merely by designating doctors as ‘consultant doctors’, hospitals cannot deduct lower TDS (on payments made/perquisites provided to doctors) under section 194J/section 194R and escape higher TDS at slab rates applicable to salaries.

Also, in case of digital platforms, the conventional test of “control and supervision by employer” would fail. There is no way a ride-hailing services or app can dictate to its onboarded or platformed drivers how they should drive the car/do their job. There is no way they can supervise it. Nor can an aggregator for plumbers, carpenters etc. dictate to its onboarded service providers how they should do the job as these are very skilled jobs. There is no way the aggregator can supervise work done. Therefore, in Uber BV and others (Appellants) v. Aslam and others (Respondents) [2021] UKSC 5, decided 20.02.2021, the UK Supreme Court, in deciding whether Uber drivers were employees of Uber or not, applied the following test laid down by the Supreme Court of Canada in McCormick v. Fasken Martineau DuMoulin LLP 2014 SCC 39; [2014] 2 SCR 108, para 23 –

“Deciding who is in an employment relationship … means, in essence, examining how two synergetic aspects function in an employment relationship: control exercised by an employer over working conditions and remuneration, and corresponding dependency on the part of a worker. … The more the work life of individuals is controlled, the greater their dependency and, consequently, their economic, social and psychological vulnerability in the workplace …”

The above test would also be relevant for determining whether a doctor is employee of the hospital or an independent professional.

3. Recipient Must Be Carrying on Business/Profession

Recipient must be carrying on business/exercising a profession. At the very least, he must be engaged in adventure in the nature of trade. Otherwise, there is no way a perquisite or benefit received can be said to arise from recipient’s business or profession.

If benefit or perquisite is to be subjected to TDS under section 194R regardless of whether recipient is carrying on any business or profession, then, Parliament would have worded the provision like clause (ii) of Explanation 3 to section 37(1) wherein the wording is “any benefit or perquisite, in whatever form, to a person, whether or not carrying on a business or exercising a profession”. Since section 194R is not worded like the said Explanation 3, it is clear that recipient must be carrying on a business or exercising a profession in order to attract section 194R.

Question No. 4 of CBDT’s Circular 12/2022, dated 16.06.2022 clarifies that

“The provision of section 194R of the Act shall not apply if the benefit or perquisite is being provided to a Government entity, like Government hospital, not carrying on business or profession”.

So long as it arises from recipient’s business or profession, it matters not as to under what head the income is taxed so long as it is not taxable under “salaries”. It is not necessary that the benefit/perquisite should be taxable in recipient’s hands only under the head “Profits and Gains from business or profession”. It may even be taxable under income from other sources (e.g. benefit or perquisite provided to a director other than Managing Director (MD)/Whole-Time Director (WTD) is taxable under the head income from other sources). If benefit/perquisite is taxable under the head “salaries” (i.e there exists employer-employee relationship between provider of perquisite/benefit and recipient), then it will be liable for TDS under section 192 and not under section 194R. If benefit or perquisite is taxable in the hands of recipient under any other head of income (e.g. profits and gains from business or profession/income from other sources), then TDS will be deductible under section 194R.

3.1 Payment Made by Company to Panchayat Samiti for Village Development/Temple Development/Compensation or Any Other Reason for the Smooth Execution of Projects. Whether TDS u/s 194R Deductible on Such Payment?

The benefit or perquisite provided would come under the TDS net of Section 194R only if it is ‘arising from’ business or the exercise of a profession by the recipient of such benefit. The causal connection suggested by the words “arising from” is that one (benefit/perquisite provided to resident recipient) originates from or springs forth or results from or proceeds as a consequence of the other (carrying out a business or the exercise of a profession by the resident recipient). The causal connection, according to judicial precedents, suggests a proximate cause. In other words, the business carried out by the resident recipient or the profession exercised by him should be the proximate cause of benefit or perquisite provided to him. The recipient (i.e., panchayat samiti) is not engaged in any business or profession. Where the recipient is not engaged in any business/profession, it cannot be said that any perquisite/benefit has arisen to him from business or the exercise of a profession.

So, it is opined that even if there is ‘providing’ of any ‘benefit’ or ‘perquisite’, the same is out of the purview of Section 194R. As the recipients cannot be said to carry on any business or profession, no perquisite or benefit can be said to arise to the recipient from business or exercise of a profession and no tax is required to be deducted under Section 194R. It will be futile to examine the questions of whether what is given is a ‘perquisite’ or ‘benefit’.

3.2 Whether Company Is Required to Deduct TDS u/s 194R on Payments Made by It Towards Donations/CSR Expenditure?

Section 194R has no application because the recipients (i.e., CSR funds or other donees) are not engaged in any business or profession.

3.3 Resident Recipient Must Be Having a Business or Professional Relationship With the Provider of Benefit/Perquisite (Deductor)

In the following instances, TDS on benefits or perquisites were held to arise from business or exercise of profession and hence held taxable under section 28(iv) –

- Where assessee, a film actress, had done promotional activity on being brand ambassador of NDTV Toyota Greenathon campaign and had clearly promoted brand Toyota, receipt of Toyota car as gift in this connection had rightly been added in her hands as perquisites under section 28(iv) [Ms. Priyanka Chopra v. Dy. CIT [2018] 89 taxmann.com 286 (Mumbai – Trib.)]

- Where assessee film actress received a watch worth ` 40 lakhs as a gift from the company for which she had undertaken advertisements and promotional activities on remuneration basis, tax authorities were justified in making an addition of said gift to assessee’s income as perquisite under section 28(iv) [Ms. Priyanka Chopra v. Dy. CIT [2018] 89 taxmann.com 287 (Mumbai – Trib.)]

In the following instances, TDS on benefits or perquisites were held to NOT arise from business or exercise of profession and hence held not taxable under section 28(iv) –

- The assessee, a film actor, received villa from Dubai based company. It was held that the mere fact that assessee attended annual day celebrations and addressed to employees of donor company, it did not amount to rendering professional services or carrying out brand endorsement activities and, thus, value of villa could not be brought to tax under sec. 28(iv). In view of the above, tax is not deductible under section 194R. [Assistant Commissioner of Income-tax, Central Circle 29, Mumbai v. Shahrukh Khan [2017] 84 taxmann.com 209 (Mumbai – Trib.)]

- Where assessee purchased shares of a non-related company at a price less than fair value as it was a loss-making concern, no benefit arose to assessee which could be brought to tax under section 28(iv). The assessee in this case purchased certain shares at a certain price from parties other than the company whose shares were acquired.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.