FAQs on Taxation of ULIPs

- Blog|Income Tax|

- 10 Min Read

- By Chetan Kulasri

- |

- Last Updated on 17 February, 2022

Latest from Taxmann

The Finance Bill, 2021 proposes to tax certain Unit Linked Insurance Plans (ULIPs). The relevant change in the taxation regime of ULIPs is proposed by withdrawing the exemption under Section 10(10D) in respect of such plans and consequently, taxing them under Section 112A of the Act.

It is proposed that no exemption under Section 10(10D) shall be available in respect of ULIPs issued on or after the 01-02-2021 if the amount of premium payable for any of the previous year during the term of the policy exceeds Rs. 2,50,000. Further, if the premium is payable by a person for more than one ULIPs, the exemption shall be available only for those policies whose aggregate premium does not exceed Rs. 2,50,000, for any of the previous years during the term of any of the policy (hereinafter referred to as ‘high premium ULIP’).

The new taxation regime of ULIPs shall apply only to those insurance policies which are issued on or after 01-02-2021. This article will answer all your questions about the taxability of the ULIPs.

1. What is a Unit Linked Insurance Plan?

Unit Linked Insurance Plan is a hybrid investment option which consists of a mix of insurance and investment to serve the needs of the respective investors. The amount of premium of a ULIP scheme is partly towards the insurance of the policyholder and partly towards the investment. The investable portion of the premium is invested in equity, debt, money market or a mix of all based on the goals and risk appetite of the investor.

2. What are the types of ULIPs?

An investor can invest in the ULIPs for his retirement planning, wealth-creation, child-education, family security, so on and so forth. ULIPs, by and large, allow options of payment of single-premium or regular premium. ULIPs based on the types of portfolios the money of insurer is invested in, can be categorized into the following:

-

- Equity-Based Funds;

- Debt-Based Funds;

- Money Market Based Funds; and

- Balanced Funds.

Dive Deeper:

Taxation of Unit Linked Insurance Plan (ULIPs)

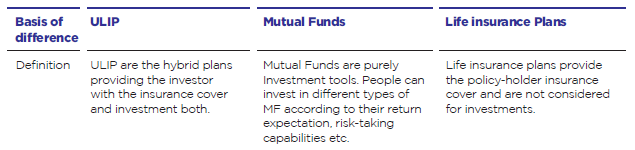

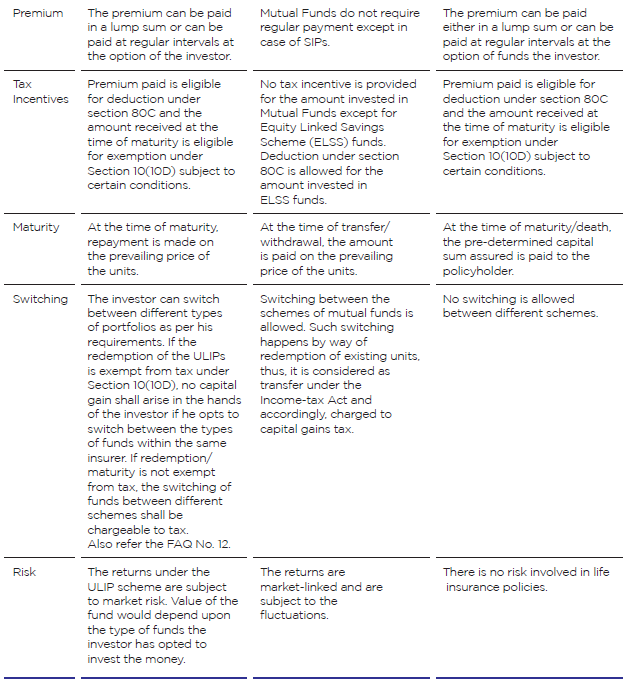

3. Difference between ULIP, Life insurance and Mutual Funds

Here are the quick difference between ULIP, Life insurance and Mutual Funds:

4. Is there any lock-in period of investment in ULIP?

ULIPs typically have a lock-in period of 5 years.

5. Whether deduction allowed under Chapter VI-A for investment in ULIPs?

Yes, deduction under Section 80C is allowed for the investment made in ULIP. An Individual can claim a deduction for the investment made for himself, spouse or children (dependent or independent) and HUF can claim a deduction for the investment made for any member of HUF.Deduction under section 80C is restricted to 10% of the actual capital sum assured. It means that if the person pays an exorbitant premium for an insurance cover, the deduction shall not be allowed for the entire premium. The deduction will be limited to 10% of the sum assured, and any amount of premium paid more than this limit is not deductible under Section 80C.Investment in ULIP is generally spread over 10 years or 15 years. The deduction is allowed only if the taxpayer contributes to ULIP for first five years of the plan. If he stops contributing in the plan before the expiry of five years or he terminates his participation by notice to that effect, the aggregate of deductions allowed to him in the earlier years shall be deemed as his income and charged to tax in the year in which such termination or cessation occurs.No changes have been proposed to Section 80C by the Finance Bill, 2021. The deduction under Section 80C shall not be allowed in the event of payment of excess premium (more than 10% of the sum insured), while as it will continue to be deductible in case of higher premium (more than Rs. 250,000). However, the deduction under Section 80C shall not exceed Rs. 1,50,000.

6. When an exemption is allowed under Section 10(10D) for the sum received under ULIP?

(Before the Budget)Section 10(10D) provides for exemption with respect to any sum received under ULIP, including the sum allocated by way of bonus on such policy. However, if the premium payable for any of the years during the term of the policy exceeds 10% of the actual capital sum assured, then no exemption under this section would be allowed with respect to the sum received under the policy. Such situation hereinafter referred to as ‘excess premium’.

7. When an exemption is allowed under Section 10(10D) for the sum received under ULIP?

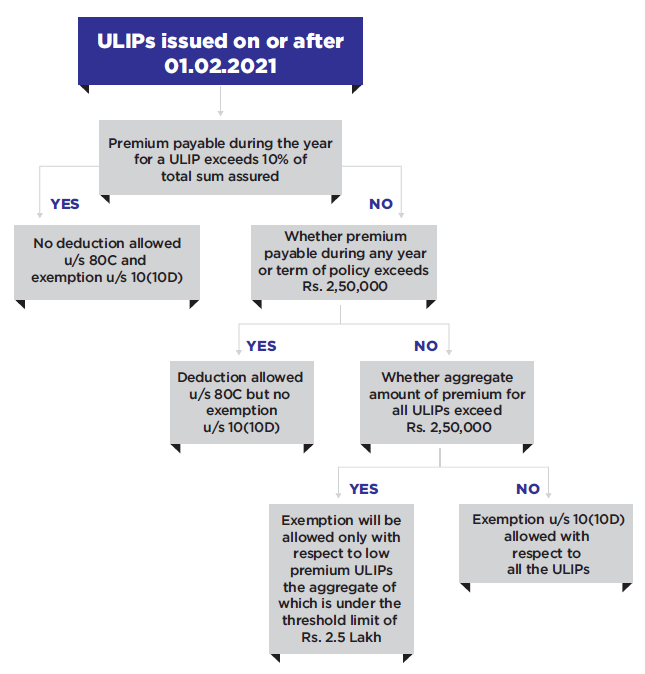

(After the Budget)Besides restricting the exemption under Section 10(10D) for payment of excess premium, the Finance Bill, 2021 has proposed to insert Fourth and Fifth Proviso to Section 10(10D) that no exemption shall be available under this provision in respect of ULIPs issued on or after the 01-02-2021, if the amount of premium payable for any of the previous year during the term of the policy exceeds Rs. 2,50,000 (i.e., ‘high premium’ ULIPs).The Fourth Proviso provides that no exemption shall be available for a policy, acquired on or after 01-02-2021, if the premium paid in any year during the tenure of the ULIP exceeds Rs. 2,50,000 (single policy). So, where premium payable for a policy exceeds Rs. 2.5 lakhs in any year during its tenure, no exemption under section 10(10D) will be allowed with respect to such policy.The Fifth Proviso provides the exemption for all those policies whose aggregate premium in any year during the tenure of the policies is less than Rs. 2,50,000 (Multiple Policies). This would imply that in case the person has more than one policy acquired on or after 01-02-2021, and the premium payable for each of such policy during any year does not exceed Rs. 2.5 lakhs but the aggregate of premium payable for all such policies exceeds Rs. 2.5 lakhs in a year, the exemption under this section would be allowed only in respect of those policies whose aggregate premium is within such prescribed limit.Thus, in other words, exemption shall be allowed only with respect to low premium ULIPs the aggregate of which is under the threshold limit of Rs. 2.5 Lakh.

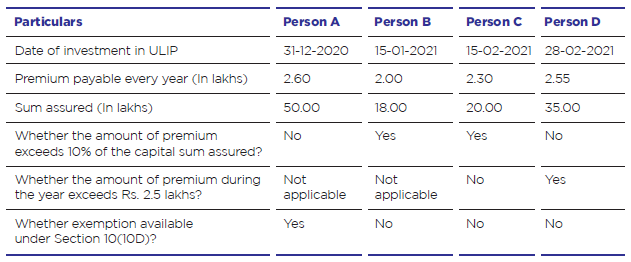

Example 1: Determine whether the exemption is available under Section 10(10D) for a single policy purchased by four different persons in the following scenarios.

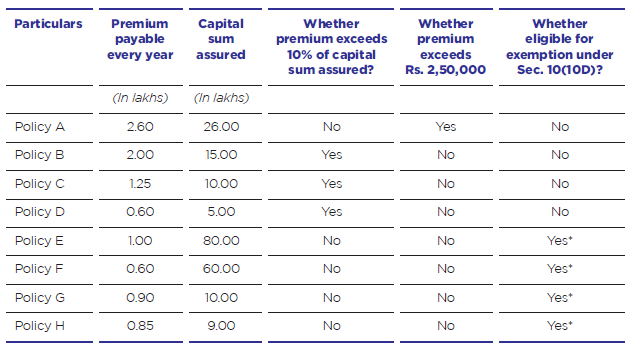

Example 2: Determine whether the exemption is available under Section 10(10D) for multiple policies purchased by one person on or after 01-02-2021 in the following scenarios.

Though the last four policies are eligible for exemption under Section 10(10D) but the exemption can be claimed in respect of only those policies whose aggregate premium during the year does not exceed Rs. 2,50,000 (i.e., low premium policies). Further, the threshold limit of Rs. 2,50,000 should be exhausted for those low premium policies first which have a higher yield. Low-yield ULIPs should be avoided from exhausting the limit of Rs. 2,50,000. It will, in turn, reduce the ultimate taxable capital gains. If the yield from such eligible policies is the same, the investor should consider Policy E, F and G as the aggregate premium of such policies equal to Rs. 2,50,000. If policy H is included, the limit of Rs. 2,50,000 cannot be exhausted fully.

8. Whether there is any change in the taxability in the event of the death of the policy-holder?

In the event of the death of the policy-holder, the exemption shall not be denied under Section 10(10D) from either of the policy, that is, excess premium policy (more than 10% of sum assured) or higher premium policy (more than Rs. 2,50,000).

9. Under which head the sum received from ULIPs shall be taxable?

As Income-tax Act does not contain any guidance on this aspect, the income arising in the event of disallowing the exemption under Section 10(10D), it used to be taxable under the head ‘capital gains’. The reasoning behind this is that when a person takes an insurance policy, he gets the right to receive sum due against his insurance policy either on maturity or on its surrender or mishappening. Therefore, the right to receive a sum from the insurance policy is a capital asset within the meaning of section 2(14) and any income or losses arising on its transfer shall be chargeable to tax under the head ‘Capital Gains’. If an insurance policy has been held for more than 36 months, it shall be considered as long-term capital assets, accordingly the benefit of cost inflation index shall be given while computing the capital gains.However, as the Finance Bill, 2021 proposes that only those ULIP shall be considered as ‘capital asset’ to which exemption under Section 10(10D) does not apply, on account of the applicability of the fourth and fifth proviso thereof. This amendment, thus, keeps only the high-premium policies within the meaning of ‘capital asset’, which, in turn, gives an impression that excess-premium policies (more than 10% of sum assured) shall not be considered as a capital asset. This does not seem to be logical but seems to be an inadvertent error. If this aspect is ignored, the proceeds from the excess premium policies shall also be taxable under the head capital gains. If not, proceeds from such excess-premium policy should be taxable as residuary income or alternatively, it could be argued that in absence of its inclusion within the meaning of ‘income’ under Section 2(24), it should be treated as capital receipts not chargeable to tax.If it is assumed that excess-premium and high-premium policies are taxable under the head capital gains, the former one will be taxable at applicable tax rates in case of short-term capital gains and at the rate of 20% with indexation in case of long-term capital gains. Whereas, the taxability of the high-premium policies will depend upon the nature of policy and chargeability of STT thereon. If such ULIPs are equity-oriented and chargeable to STT, the tax shall be levied at the rate of 15% in case of short-term capital gain (section 111A) and at the rate of 10% in case of long-term capital gain (Section 112A). In other cases, the taxability shall be same as in case of excess premium policy (for more details about the tax rates applicable in case of excess-premium and high premium policies, refer to Question 11).

10. How much amount shall be charged to tax under the head capital gains?

The Finance Bill, 2021 proposes to insert a new sub-section (1B) to Section 45 to provide that where any person receives at any time during any previous year any amount under a ULIP, to which exemption under Section 10(10D) does not apply on account of the fourth and fifth proviso thereof, including the amount allocated by way of bonus on such policy, then, any profits or gains arising from receipt of such amount by such person shall be chargeable to tax under the head “Capital gains” in the previous year in which such amount was received. Further, the income taxable under this head shall be calculated in such manner as may be prescribed. Thus, the manner of computation of income shall be notified subsequently.

11. How much is the tax rate on such capital gains?

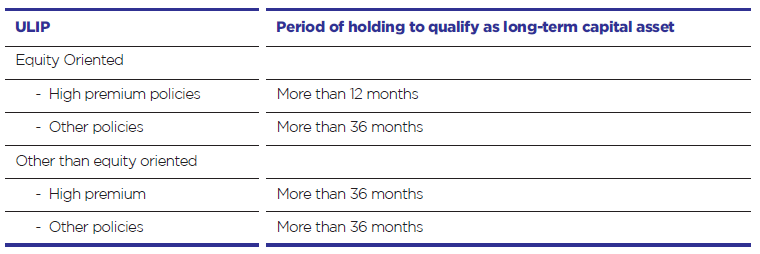

The definition of ‘Equity Oriented Fund’ in Section 112A is proposed to be amended by the Finance Bill, 2021. It is proposed to cover ULIPs to which exemption under Section 10(10D) does not apply on account of the applicability of the fourth and fifth proviso thereof. The said definition contains a condition that atleast 65% of the total proceeds of such ULIPs in the equity shares of domestic companies listed on a recognised stock exchange. This condition shall continue to apply to a ULIP policy for its taxability under this provision. Thus, only High Premium Equity-Oriented ULIPs shall be taxable under Section 112A or Section 111A, as the case may be. Gains arising from other ULIPs (debt based, balanced, etc.) shall be taxable as per general provisions.The tax rate on the capital gains depends upon the nature of capital asset (short-term or long-term), which is determined on the basis of its period of holding. A capital asset is generally treated as long-term capital asset if it is held for more than 36 months immediately preceding the date of its transfers otherwise the same shall be treated as short-term capital assets. However, the period of 36 months is treated as 12 months in case units of Equity-Oriented Fund. The period of holding to determine long-term or short-term capital gain after the amendment proposed by Finance Bill, 2021 shall be as follows:

Once the nature of capital gain is determined on basis of period of holding of ULIPs, the tax rate shall depend upon the type of ULIP and the chargeability of STT thereon. This can be explained with the help of following flow charts:

12. What is Fund Switching in ULIPs?

In the ULIPs, the policyholders have an option to switch between different types of funds (equity, debt, money-market or balance) or allocate money in a variety of funds. They can opt to switch the investment funds fully or partially into different portfolios according to their future needs and their risk appetite. As per the IRDA (Unit Linked Insurance Products) Regulations, 2019, the investment pattern can be switched by moving from one segregated fund either wholly or partly to other segregated funds amongst the segregated funds offered under the underlying Unit Linked insurance product of an insurer. There are generally no charges applicable for switching between the types of funds. Many insurers provide a particular number of free switches a person can make within a year, and additional charges are applicable in case he opts to switch beyond that limit.No tax implications would arise on such switching from one fund to the other provided the maturity/redemption of units of ULIPs are exempt under Section 10(10D). If no such exemption is available for the excess premium or high-premium policies, such switching between the funds may be taxable under the head capital gains. However, the CBDT should provide clarity on this aspect.

13. Whether STT be levied on transfer/ redemption of ULIPs?

STT is required to be collected by the trustee or any other managing the funds in case of mutual funds or recognised stock exchange in case of any other specified securities transacted through a recognised stock exchange.Finance Bill, 2021 has proposed to amend various provisions under Finance (No. 2) Act, 2004 to enable levy of STT on amount received by the policyholder at the time of maturity or partial withdrawal with respect to ULIPs issued on or after 01/02/2021. Levy of tax in case of ULIPs has been brought on the similar lines as in case of equity oriented mutual fund units issued in respect of ULIPs. STT will be levied if all the following conditions are satisfied:

-

- The ULIP is issued on or after 01/02/2021

- Policyholder has transferred units of equity oriented funds issued by the insurer with respect to ULIPs;

- Amount is received due to sale or surrender or redemption of the units on account of maturity or partial withdrawal.STT will be levied at the rate of 0.001% on the value of transaction and is required to be paid by the seller of the units. Amendment in other provisions regarding furnishing of return and collection and recovery of STT has also been proposed by ensuring the same provisions are applicable in case of above mentioned ULIPs and equity oriented mutual funds.

Disclaimer: The content/information published on the website is only for general information of the user and shall not be construed as legal advice. While the Taxmann has exercised reasonable efforts to ensure the veracity of information/content published, Taxmann shall be under no liability in any manner whatsoever for incorrect information, if any.